Let’s de-mystify compounding with real numbers you can feel in your gut, not just nod at.

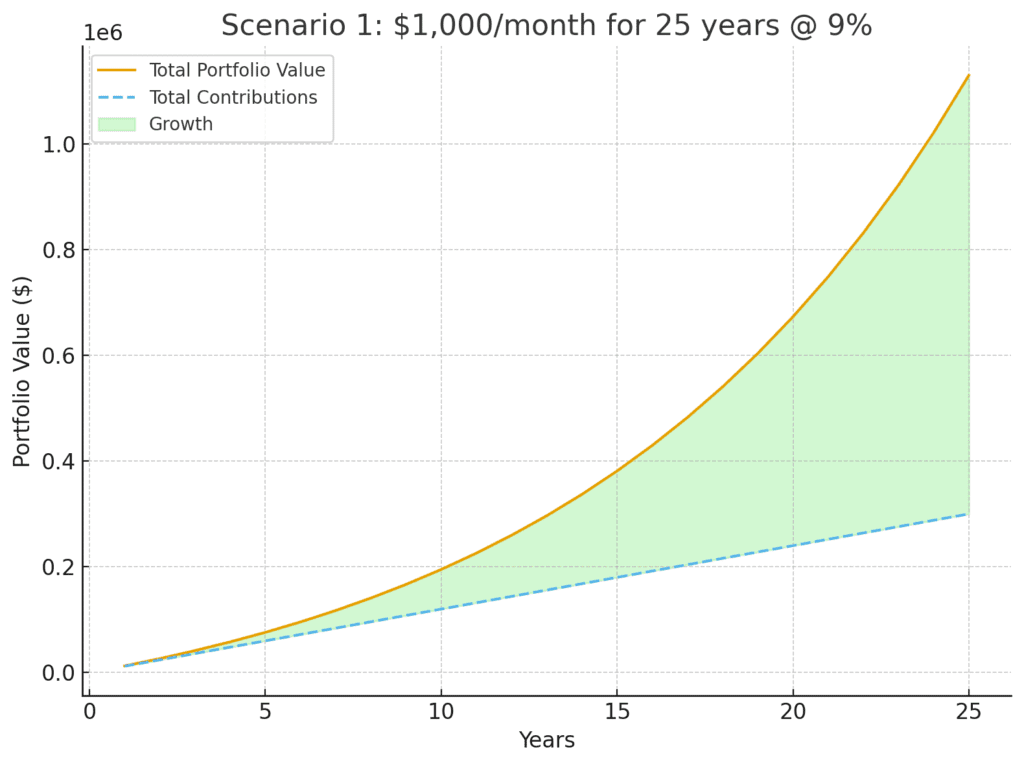

The $1,000/month for 25 years example

- Your contributions: $1,000 × 12 × 25 = $300,000.

- Potential outcome at ~9% average: ~$1,121,000.Growth (what your money earned): ~$821,000.

Read that again. Roughly 73% of the final million isn’t the cash you put in—it’s the growth on your growth.

That’s compounding.

Analogy time: Imagine planting a small garden. In year one you harvest a little. You save the seeds and plant them again—with last year’s seeds plus the new ones. Fast-forward and your garden looks “unfair.” It’s not. You just let the seasons do their thing, over and over.

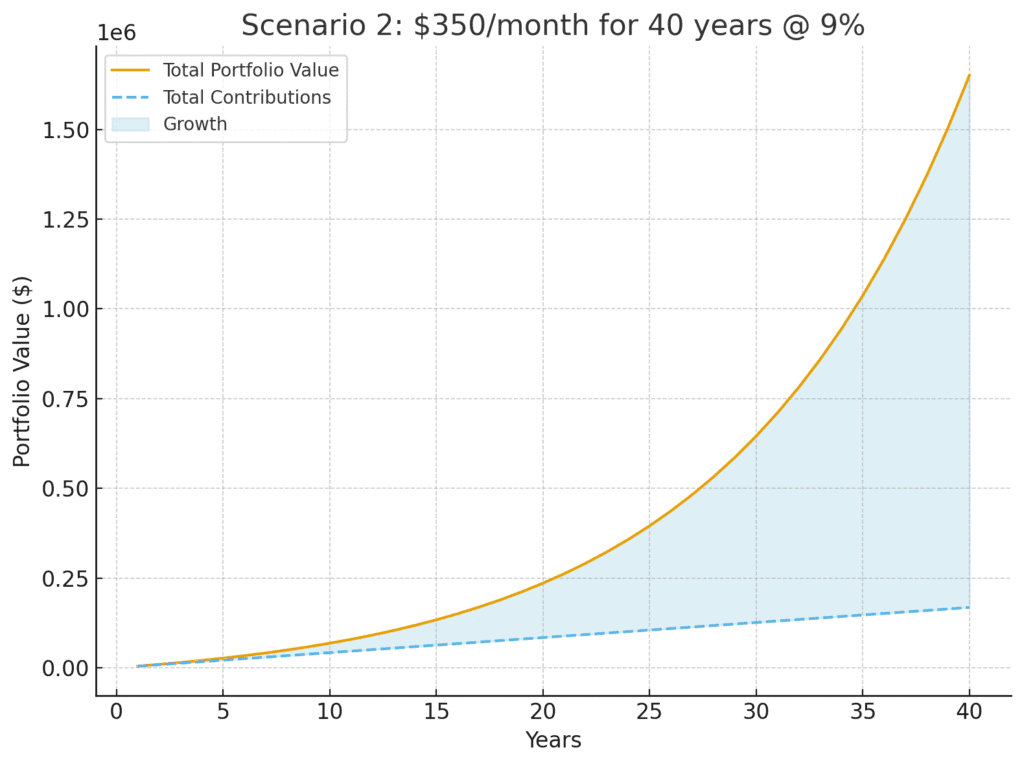

“I’m starting younger—what if I only have $350/month?”

Perfect. Starting early is like putting your garden on a sunnier slope.

- Your contributions: $350 × 12 × 40 = $168,000.

- Potential outcome at ~9% average: ~$1,638,000.

- Growth: ~$1,470,000 (about 90% of the total!).

Even if returns average closer to 8%, you’re still around $1.22M.

At 7%, you land just under $920K—still life-changing for most households, especially inside a TFSA/RRSP where the tax treatment compounds the benefit.

Key insight: the earlier you start, the less you personally have to contribute to reach a big number, because time does more of the heavy lifting.

Why “capital vs. growth” matters (and motivates)

Most people think wealth comes from brutally high savings rates. And yes, a healthy margin matters. But the engine is time in the market. Showing the split between what you put in (capital) and what the market added (growth) reframes investing from “I have to pinch pennies forever” to “I need a system that buys me time.”

Here’s that split, side-by-side:

- $1,000/month × 25 years @9% → $300K contributed / ~$821K growth

- $350/month × 40 years @9% → $168K contributed / ~$1.47M growth

The takeaway isn’t “aim for 9% every year” (you won’t). It’s “get invested, stay invested, and let compounding have a long runway.” In Canada, prioritize TFSA for tax-free growth and use RRSP strategically (especially if you’re in a higher tax bracket today than you expect in retirement).

A quick reality check (because I refuse to sell fairy tales)

- Returns aren’t linear. You won’t get a smooth 8–9% every year. Some years are ugly. That’s normal.

- Currency matters. If you use a Canadian ETF that tracks the S&P 500, CAD/USD moves will impact returns in CAD terms. Over long periods, the equity risk dominates, but it’s worth noting.

- Fees matter. An extra 1–2% in fees is a quiet thief. Use low-cost index ETFs to keep more of your growth.

A tiny story to make it real

Two friends—Amira and Dan—both want seven figures by 65.

- Amira starts at 25 with $350/month. She invests through her TFSA automatically on payday. She forgets about it (on purpose).

- Dan waits until 40 to “start seriously.” He puts in $1,000/month and tells himself he’ll “catch up later.”

At 65, Amira, the “small but early” investor, didn’t just catch up—she likely lapped Dan. Not because she’s a genius. Because she let time be her teammate for an extra 15 years.

“But what if I can’t find $1,000—or even $350—right now?”

That’s where the rest of this article goes next: creating investable margin. If your income is under ~$60K, your lever is earn more (not micro-cutting joy from your life). If your income is over $100K and you still can’t find surplus, your lever is simplify fixed costs (mortgage/car/insurance). Different problems, different solutions. Same outcome: free up dollars, automate them into your TFSA/RRSP, and let compounding start the clock.

Micro-moves you can make this month (so momentum starts now)

- Automate a small transfer (even $100) into a TFSA-eligible index ETF. Let the habit precede the amount.

- Name your money: “Rent,” “Groceries,” “Investing,” “Fun.” Money with a job behaves better.

- Turn raises into contributions: every salary bump, increase the auto-transfer before you feel the lifestyle creep.

- Know your fee: if you’re paying >0.50% in fund fees, you’re likely donating future you’s money.

The punchline

Compounding is a force of nature disguised as boring math. The magic isn’t “picking winners.” It’s time × consistency × low friction. Your job is to set up a system that runs whether you’re motivated or not.

In the next section, we’ll separate two very different situations—and give each its own playbook:

- Income is the bottleneck (typically under ~$60K): how to raise the ceiling without burning out.

- Fixed costs are the bottleneck (often $100K+ earners): how to unlock margin without feeling deprived.

Because the worst strategy is to wait and do nothing. The best strategy is to start—small if you must—and let time do what time does.